NeoBit Daily

NeoBit Daily

As cyber threats continue to evolve rapidly, businesses and individuals alike are turning to cybersecurity insurance as a critical layer of protection for data privacy. In 2026, the landscape of these policies is shifting dramatically in response to sophisticated hacking techniques and stringent regulatory requirements. This comprehensive guide explores the latest trends, identifies potential coverage gaps, and provides actionable advice for securing optimal protection while integrating insurance into broader cybersecurity frameworks.

The Rising Importance of Cybersecurity Insurance in 2026

Cybersecurity insurance has become indispensable due to the increasing frequency and severity of data breaches across industries. Organizations must integrate these policies into broader data privacy strategies to mitigate financial and reputational damage from incidents that can disrupt operations for weeks or months. Regulatory bodies worldwide are enforcing stricter compliance standards, making insurance not just a safeguard but often a necessity for continued operations in sectors like finance, healthcare, and retail. The interconnected nature of global supply chains means that a single breach can cascade into widespread liability, underscoring why companies are prioritizing policies that cover both direct losses and third-party claims. Without adequate coverage, even well-prepared organizations risk insolvency following a major incident.

Adapting to New Hacking Techniques and Regulatory Demands

Hackers are leveraging advanced AI-driven attacks, polymorphic ransomware, and supply-chain compromises that specifically target IoT ecosystems and cloud infrastructures. Insurance providers are updating policies to address these evolving threats while aligning with regulations such as updated data protection frameworks from international standards bodies. Policies now frequently require evidence of proactive security measures, including continuous monitoring and employee training programs, before coverage is extended or renewed. This adaptation ensures that insurers remain viable while encouraging policyholders to maintain higher security baselines. Companies that fail to demonstrate compliance with emerging regulatory demands often face higher scrutiny during underwriting or outright policy denials.

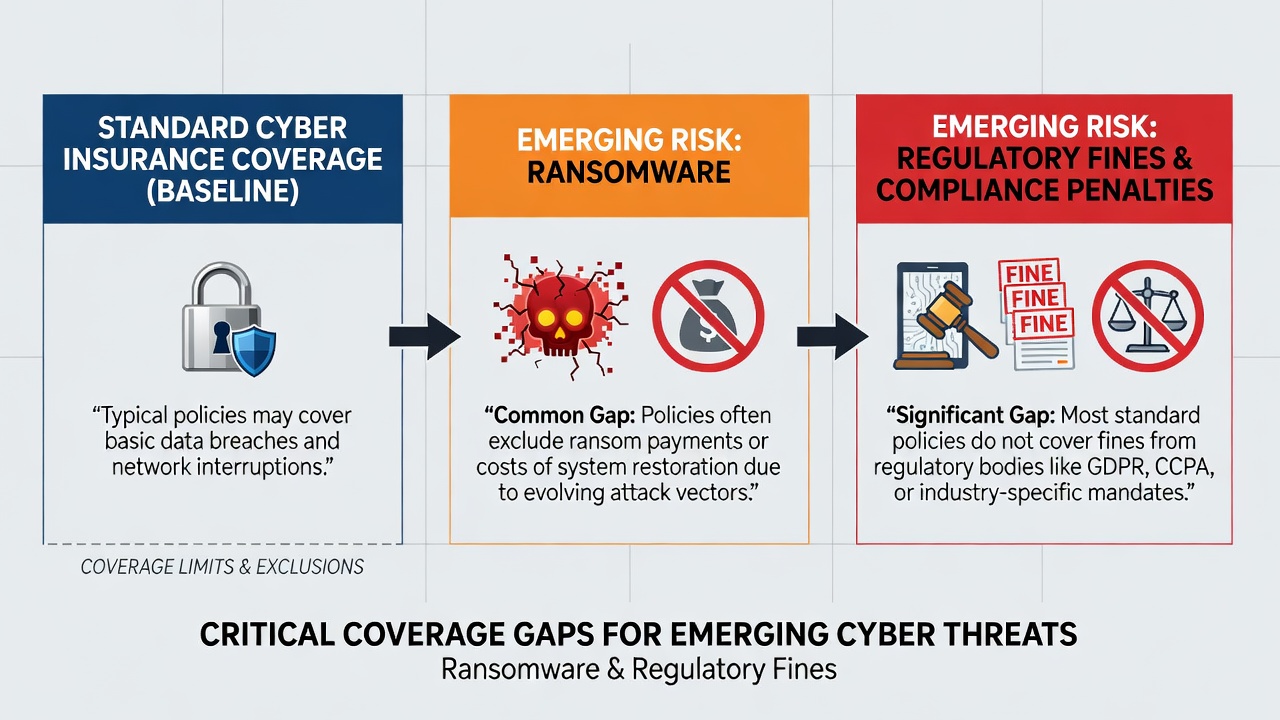

Coverage Gaps for Emerging Risks

Despite advancements in policy design, many standard agreements still fall short on emerging risks such as quantum computing vulnerabilities that could decrypt current encryption standards or deepfake-enabled social engineering campaigns that bypass traditional verification. It is essential to review exclusions related to state-sponsored attacks, nation-state actors, and third-party vendor liabilities that may not trigger full payouts. Understanding these gaps helps organizations supplement insurance with additional technical controls and layered defenses. For instance, policies may exclude losses from unpatched legacy systems or failures in multi-factor authentication implementation, leaving significant exposure that requires separate risk management strategies.

Steps to Qualify for Better Premiums

To secure favorable terms and conditions, companies should implement robust security frameworks that demonstrate maturity to underwriters. Key steps include conducting regular risk assessments by independent auditors, achieving recognized certifications such as ISO 27001, and maintaining documented incident response plans that outline clear escalation procedures. Insurers often reward organizations that demonstrate strong data encryption practices across all data flows, comprehensive employee training programs on phishing recognition, and regular tabletop exercises simulating breach scenarios. Additional qualifying actions involve deploying endpoint detection tools and establishing vendor risk management programs that extend security requirements to partners.

- Perform annual penetration testing and vulnerability scans with remediation tracking.

- Adopt multi-factor authentication across all systems and enforce least-privilege access controls.

- Establish clear data breach notification protocols aligned with regulatory timelines.

- Partner with certified cybersecurity vendors for ongoing monitoring and threat intelligence sharing.

- Document all security policies and conduct annual reviews with executive oversight.

Comparing Top Providers

Leading insurers differentiate themselves through specialized add-ons for regulatory fines, business interruption coverage, and post-breach services such as credit monitoring for affected individuals. Evaluation should focus on claim processing speed, customization options for industry-specific needs, and seamless integration with existing security tools rather than relying on generic marketing comparisons. Prospective buyers benefit from requesting sample policy wordings and reviewing historical claim resolution data to understand real-world performance. This detailed comparison process helps identify providers that truly align with an organization's risk profile and operational realities.

Real-World Case Studies of Data Breach Claims

One notable example involves a mid-sized retailer that successfully claimed under its policy after a ransomware attack exposed customer payment data. The insurer covered forensic investigations, regulatory penalties, and notification costs, highlighting the value of comprehensive riders that include crisis management support. The organization had maintained detailed logs and an updated incident response plan, which expedited the claims process and minimized downtime. Another case featured a healthcare provider whose proactive security posture, including regular penetration tests and employee awareness training, led to faster claim approval and reduced out-of-pocket expenses following a phishing-induced breach of patient records. A third scenario saw a manufacturing firm navigate a supply-chain compromise where insurance covered both direct recovery costs and downstream liability to affected partners, demonstrating how thorough policy reviews can prevent disputes over shared responsibility.

Practical Security Tips for Policyholders

Policyholders can enhance their protection by combining insurance with technical and procedural measures that reduce the likelihood of incidents occurring in the first place. Regular audits of network perimeters, adoption of zero-trust architectures that verify every access request, and sustained employee awareness campaigns are proven strategies that also strengthen insurance applications. Additionally, reviewing policies annually ensures alignment with the latest threat landscape and any new regulatory developments. Organizations should maintain offline backups, segment networks to limit lateral movement during attacks, and establish relationships with incident response firms before a breach occurs.

Integrating Insurance with Overall Cybersecurity Strategies

Effective integration requires viewing insurance as one component within a defense-in-depth model rather than a standalone solution. This means mapping policy coverage directly to identified risks from formal assessments and ensuring that technical controls address the gaps that insurance cannot fully cover. Regular joint reviews between security teams and risk management professionals help maintain this alignment. Resources from authoritative organizations provide frameworks for building these integrated approaches. For example, guidance available at NIST offers detailed control catalogs that align well with insurance underwriting criteria, while CISA publishes alerts and best practices that policyholders can implement to demonstrate due diligence.

Conclusion

Navigating cybersecurity insurance in 2026 requires a proactive stance on data privacy that combines policy selection with ongoing security improvements. By understanding current trends, addressing coverage gaps through careful review, and following best practices outlined above, organizations can build resilient defenses that complement their insurance investments. Staying informed through authoritative resources such as NIST and CISA ensures ongoing compliance and protection against an ever-changing threat environment.

FAQ

How does cybersecurity insurance integrate with overall strategies?

It serves as a financial backstop while technical controls handle prevention and detection, creating a layered defense approach that reduces both the probability and impact of incidents. Organizations achieve the best outcomes when insurance requirements directly inform security roadmaps and vice versa.

What emerging risks are typically excluded?

Many policies exclude nation-state attacks, certain AI-generated threats, and losses from unpatched systems unless specifically endorsed through additional riders. Policyholders should request explicit clarification on these exclusions during the underwriting process.

Can small businesses afford adequate coverage?

Yes, tailored policies exist for smaller entities, often with scalable premiums based on risk profiles and demonstrated security maturity. Starting with core coverage for data breaches and gradually adding modules as the business grows is a common approach.

How often should policies be reviewed?

Annual reviews are recommended, especially after major security upgrades, regulatory changes, or significant business expansions that alter the risk profile. More frequent check-ins may be warranted following high-profile industry incidents.

No comments yet. Be the first!